Financial Times 2/3/2026

Current state of the market

FINANCE

t.furgeson

2/3/20264 min read

The Current State of the Markets in Early February 2026: Resilience in Stocks Amid Volatility in Crypto and Precious Metals

As of February 3, 2026, global financial markets are exhibiting a classic tale of divergence. Major U.S. stock indices hover near all-time highs after a solid start to the year, buoyed by resilient economic data and broad-based participation. Meanwhile, Bitcoin has entered a corrective phase with sharp pullbacks and liquidations, and precious metals like gold and silver have experienced extreme volatility—parabolic rallies followed by dramatic reversals.

This environment reflects intersecting forces: Federal Reserve policy uncertainty following the nomination of Kevin Warsh as Chair (viewed as less dovish), ongoing geopolitical tensions (notably U.S.-Iran dynamics affecting oil), stretched valuations in AI/tech sectors, and shifting risk sentiment. Investors are rotating toward value and cyclicals while risk assets like crypto and high-beta metals face profit-taking. The U.S. economy shows strength—strong manufacturing data helped spark a rebound on February 2—but higher Treasury yields and a firmer dollar have pressured long-duration and speculative assets.

U.S. Stock Market: Near Records with Improving Breadth

The major indices kicked off February on a positive note after a mixed January. On February 2, the S&P 500 rose 0.5% (37.41 points) to close at 6,976.44, snapping a three-day losing streak and finishing just shy of its recent all-time high. The Dow Jones Industrial Average surged 1.1% (+515 points) to 49,407.66, briefly touching new intraday highs earlier. The Nasdaq Composite gained 0.6% to 23,592.11.

Year-to-date through early February, the S&P 500 is up approximately 1.9%, the Dow 2.8%, and the Nasdaq 1.5%. Recent trading saw intraday volatility, with the S&P 500 dipping toward 6,897–6,920 levels on February 3 amid tech rotation and yield pressures, but the overall trajectory remains upward.

A notable positive is market breadth: Around 63% of S&P 500 stocks are outperforming the index, a rare occurrence that historically signals healthier rallies beyond mega-cap tech dominance. Sectors like consumer staples, industrials, and pharmaceuticals have shown resilience, while AI/semiconductor names (Nvidia, Broadcom) faced profit-taking due to valuation concerns and questions over the pace of large AI investments.

Drivers include strong January manufacturing data, resilient corporate earnings (with mixed results from tech but positives elsewhere), and expectations around Fed policy. The Fed held rates at 3.50%–3.75% recently, with Chair Powell highlighting economic resilience and stubborn inflation, tempering aggressive rate-cut hopes. Warsh's nomination reinforced a more cautious stance on easing.

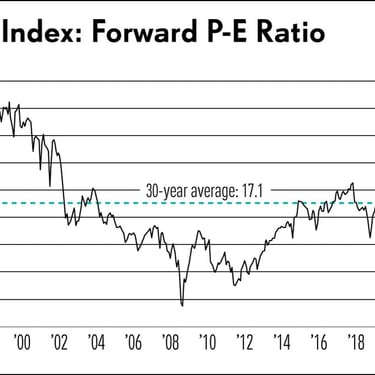

Risks persist: Higher long-term yields (10-year around 4.2%) raise discount rates for growth stocks; geopolitics and tariffs add uncertainty; and stretched forward P/E ratios (recently above 22 vs. 30-year average ~17) invite caution.

Bitcoin and Cryptocurrencies: Corrective Phase with Liquidations

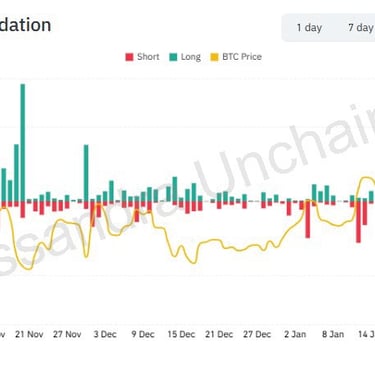

Bitcoin has been under significant pressure, trading in the $75,000–$78,000 range recently after dropping below $80,000 (first time since April 2025) and hitting weekend lows near $74,000–$75,000. As of early February 3 trading, BTC hovered around $76,000–$77,000, down roughly 2% in 24 hours and more over the week, with over $2.5 billion in liquidations (longs and shorts). Ether fared worse, down ~4–5%.

The pullback stems from risk-off sentiment spilling over from equities and metals, thin weekend liquidity, institutional outflows, disappointing tech earnings (e.g., Microsoft Azure), and broader repricing of liquidity/rate outlooks. Analysts note sensitivity to macro headwinds; some see a potential short-term bottom near $70,000, while longer-term forecasts remain optimistic ($100,000+ by year-end for some, driven by ETF adoption, institutional interest, and halving cycle echoes).

Bitcoin's market cap has shed over $200 billion recently, highlighting its high-beta nature. While some call the current phase a "bear market" or extended correction from 2025 highs, structural tailwinds like spot ETF inflows (despite recent mixed flows) and potential regulatory clarity persist. Volatility remains elevated, with thin liquidity amplifying moves.

Precious Metals: Parabolic Rally, Sharp Correction, Then Rebound

Gold and silver delivered one of the most dramatic episodes in recent memory. Both surged to record highs in late January 2026—gold above $5,000–$5,625/oz and silver over $120–$121/oz—fueled by safe-haven demand amid geopolitics (U.S.-Iran tensions, tariffs threats), central bank buying, a weaker dollar earlier, and Fed uncertainty. Gold posted massive 2025 gains (~64%+ from start to end per some settlement data).

Then came the unwind: Silver plummeted 25–30% in a single day (its worst since 1980), gold dropped 9–13%. Profit-taking, a firmer dollar/yields post-Warsh nomination, and broader risk-off flows (correlating with tech/crypto) triggered the cascade. Prices briefly stabilized lower (gold ~$4,675–$4,700, silver ~$73–$76) before rebounding sharply—gold up ~6–7% to near $4,970, silver ~8–10% to $81–$85+ on February 3.

Silver's amplified moves reflect its dual role (industrial demand + monetary). Long-term bullish factors include structural deficits, green energy demand, and gold's historical hedge properties. Short-term, technical show oversold rebounds but lingering bearish bias below key EMAs. Central banks and portfolio diversification continue supporting gold.

Other Assets and Broader Context

Oil prices swung wildly: Surging on U.S.-Iran escalation (Brent briefly >$70–$71), then plunging ~4–5% to ~$62–$66 WTI as Trump signaled talks with Iran, easing risk premiums amid broader commodities selloff. Bonds saw record issuance ($260B+ early-year global sales); 10-year yields ~4.2%. The dollar weakened at times but firms on policy shifts.

Outlook and Investor Implications

Markets in early 2026 reward selectivity. Stocks demonstrate underlying strength via breadth and economic resilience, but valuations, rates, and geopolitics warrant caution—diversification beyond mega-caps is key. Bitcoin offers high-upside potential but demands risk tolerance amid corrections. Precious metals remain volatile safe-havens, best as portfolio hedges rather than short-term trades.

Catalysts ahead include Fed communications, Q4/ongoing earnings, inflation prints, tariff developments, and Middle East dynamics. History shows such divergences often precede rotations or consolidations. Investors should monitor yields, dollar strength, and risk sentiment closely. While no one predicts perfectly, a balanced approach—equities for growth, alternatives for hedges—fits the uncertain landscape.